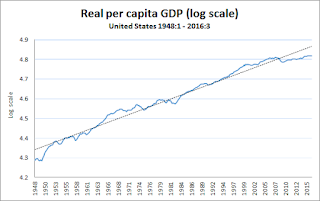

Here's the picture of real per capita GDP growth in the postwar United States.

While this is an impressive record of economic development, the recent trajectory away from (log-linear) trend has many people concerned. I share this concern. But I sometimes wonder whether the assumption of (log-linear) trend does not distort our view a little bit. In particular, one might alternatively view the pattern of economic development as "naturally" alternating between episodes or more or less rapid growth, kind of like this...

While this is an impressive record of economic development, the recent trajectory away from (log-linear) trend has many people concerned. I share this concern. But I sometimes wonder whether the assumption of (log-linear) trend does not distort our view a little bit. In particular, one might alternatively view the pattern of economic development as "naturally" alternating between episodes or more or less rapid growth, kind of like this...

This representation of "trend and cycle" is a little disconcerting in that it suggests that there is no obvious reason to expect "mean-reverting growth" any time soon. On the other hand, perhaps there is some comfort to be drawn as well. In particular, we've been there before and we somehow managed--not only to survive--but also recover. (Related post: Secular stagnation then and now).

In today's post, I want to look a little more closely at that recovery phase. While I think that a growth recovery is in the cards at some point, I'm not sure we should be expecting it to be as robust as what we experienced in the immediate postwar period or in the 1980-90s. The latter growth episode in particular was driven at least in part by a demographic force that appears to have largely dissipated. The pop in epop has popped, so to speak:

Whatever drives secular growth, it obviously cannot rely on an ever-rising employment-to-population ratio (EPOP). But EPOP can nevertheless rise for decades, as it did in the 1975-2000 period, giving the impression of secular (rather than transitory) growth.

How much did the transitory increase in EPOP contribute to GDP growth? To get a rough answer for this question, suppose that EPOP remained fixed at 58% throughout the entire sample period and subtract the amount (EPOP(t) - 0.58)*GDP(t) from the actual real per capita GDP at date t. Here's what we get:

That is, unlike the economic boom of the immediate postwar period, the more recent 80-90s boom was driven in part by a pop in EPOP. For those that prefer a log scale:

Viewed from this perspective, the growth spurt beginning in the early 1980s does not look as impressive, though it's still pretty good. And unless there's reason to believe that a similar pop in EPOP is in store in the near future, it might be prudent to scale back our forecasts for longer-term economic growth accordingly.

This representation of "trend and cycle" is a little disconcerting in that it suggests that there is no obvious reason to expect "mean-reverting growth" any time soon. On the other hand, perhaps there is some comfort to be drawn as well. In particular, we've been there before and we somehow managed--not only to survive--but also recover. (Related post: Secular stagnation then and now).

In today's post, I want to look a little more closely at that recovery phase. While I think that a growth recovery is in the cards at some point, I'm not sure we should be expecting it to be as robust as what we experienced in the immediate postwar period or in the 1980-90s. The latter growth episode in particular was driven at least in part by a demographic force that appears to have largely dissipated. The pop in epop has popped, so to speak:

How much did the transitory increase in EPOP contribute to GDP growth? To get a rough answer for this question, suppose that EPOP remained fixed at 58% throughout the entire sample period and subtract the amount (EPOP(t) - 0.58)*GDP(t) from the actual real per capita GDP at date t. Here's what we get:

That is, unlike the economic boom of the immediate postwar period, the more recent 80-90s boom was driven in part by a pop in EPOP. For those that prefer a log scale:

Viewed from this perspective, the growth spurt beginning in the early 1980s does not look as impressive, though it's still pretty good. And unless there's reason to believe that a similar pop in EPOP is in store in the near future, it might be prudent to scale back our forecasts for longer-term economic growth accordingly.

0 nhận xét:

Đăng nhận xét