|

| Japanese Prime Minister Shinzo Abe |

This is the second time in the last decade that Japan has experimented with QE (quantitative easing). How did the experiment work out in the past? And is there any reason to believe that the outcome will be different this time around?

Let's begin by taking a look at the supply of base money in Japan (Jan 1980 - Oct 13).

The first QE program started in March 2001 and ended in 5 years later in March 2006. The second QE program is evident from the chart.

According to this source, the original QE program had four goals: (1) stabilize the banking sector; (2) lower long-term interest rates; (3) increase inflation expectations; and (4) stimulate bank lending. Evidently, the program had some success with (1) and (2), but failed with (3) and (4).

Here is how core inflation behaved in Japan over the period 1992-2012:

So basically just a moderate deflation since 2000. Is this a bad thing? The conventional wisdom seems to think so. For example, here is Barry Eichengreen on the subject:

Recall that deflation wreaks its damage by discouraging spending – investment spending in particular. No one questions, therefore, that putting Japanese prices on a gradual upward trend is needed to encourage growth.Hmm, I find these to be rather odd statements, especially from an excellent economic historian. Theoretically, it is doubtful that a moderate expected deflation (or inflation) is really that harmful (it's the large unanticipated swings that potentially hurt). Here is some work by another set of fine economic historians on the subject: Good vs Bad Deflation: Lessons from the Gold Standard Era.

But never mind Gold Standard eras. What about Japan? As I've pointed out here, Japan actually experienced a robust boom in private investment spending from 2002-2008 (as part of the so-called Koizuma boom). So I'm not entirely sure what Eichengreen is on about here.

Let me reproduce my chart for real GDP in Japan:

To my eye, it looks like Japan was basically getting back on track after the interruption of the Asian financial crisis in 1997. In fact there are signs of accelerating growth in the two years leading up to the 2008 financial crisis. Did Japan's QE policy have anything to do with the Koizuma boom? I can hardly see how. The massive injection of cash was removed in 2006 with no noticeable impact on real economic activity (or inflation, for that matter).

Why didn't the original QE have an impact on inflation? We could talk all day about this. Let's start by looking at a broader measure of money: M2 (currency in circulation plus bank deposit liabilities).

Bank liabilities are created whenever a bank makes a new loan (the liabilities are destroyed whenever a bank loan is repaid). Because bank liabilities are used widely in making payments, they are money. Thus, the red line in the figure above -- the growth rate in M2 -- largely captures the growth rate in bank lending activity. As you can see, the growth rate of M2 is much lower and much more stable than the growth rate in the money base.

To a first approximation, it seems that the effect of QE is on bank reserves and not on currency in circulation/bank lending (sound familiar?). Here is the money multiplier (M2 divided by base money) in Japan:

But on the other hand, maybe this time is a bit different; at least, in terms of inflation expectations. Here are some market-based measures of inflation expectations in Japan (based on the expectations implied by comparing the yields on nominal Japanese government bonds and their inflation-protected counterparts at various maturities).

Here, we only have the 10-year inflation expectation going back to 2004 (it ends some time in 2008 and reappears right at the end of the sample there at about 1%). I've plotted all available maturities here to give us the broad picture. As with the U.S., inflation expectations took a dive during financial crisis (see here). While inflation expectations have been trending upward since before Abe took office, it is notable that they have continued to climb significantly past 1%.

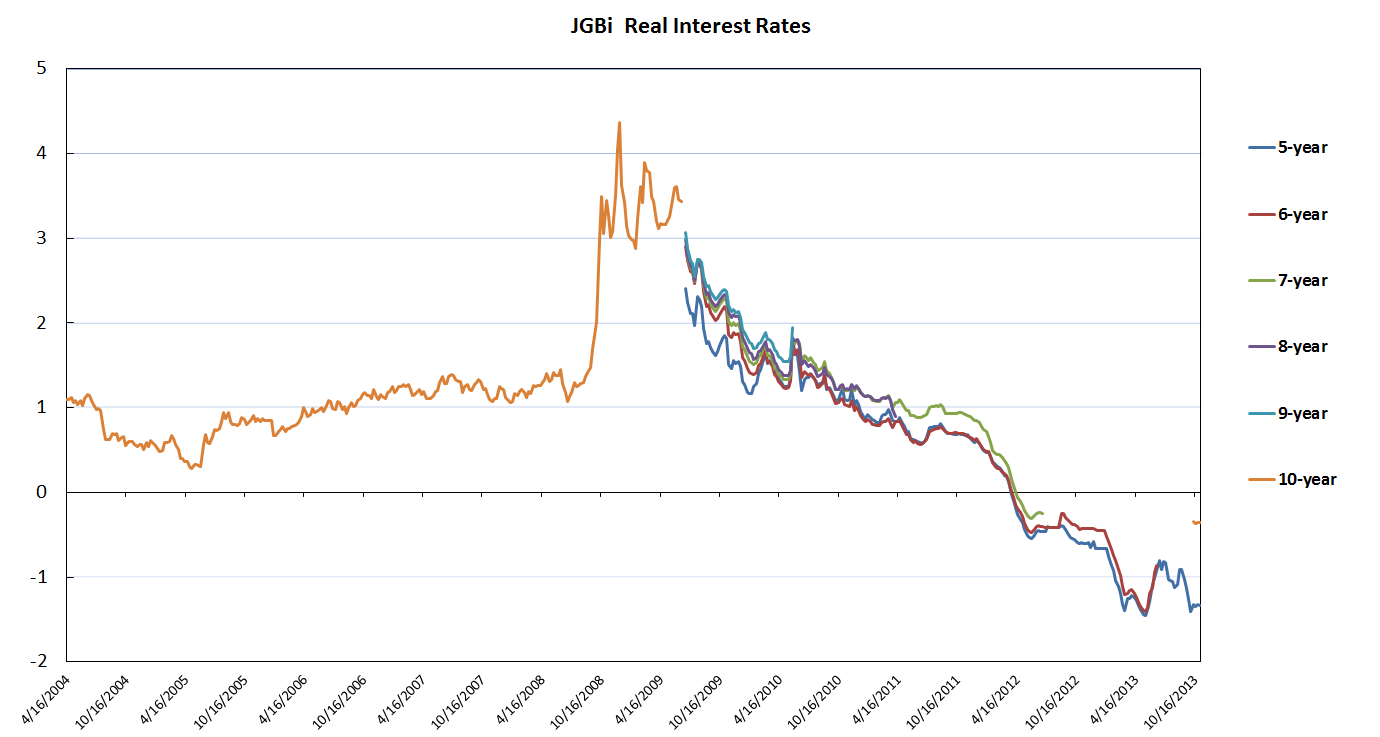

Here is a plot of the expected real interest rate on Japanese government bonds at different maturities:

So it appears that Abeconomics has "succeeded" in driving the real interest into negative territory. I suppose this is a good thing if for some reason the market "wants" negative real rates, but is prevented from achieving them owing to the zero lower bound on nominal interest rates.

But the deeper question is: Why do real rates want to be so low? And why should we expect a resumption of "normal" economic activity once these negative real rates have been achieved?

Data source for Japanese inflation expectations: Bloomberg

0 nhận xét:

Đăng nhận xét